Form I-864 · Part 6, Item 7

I-864 Self-Employed Sponsor (Part 6, Item 7): How to Report Income in 2026

If you are self-employed and sponsoring your spouse, Part 6, Item 7 of Form I-864 (the affidavit of support, where you, the U.S. citizen or green card holder petitioner, promise to support your immigrant spouse, the beneficiary) asks for your current individual annual income. Your figure comes from your tax return, not from a separate calculation.

Most self-employed marriage-based sponsors

Report the Total Income line from your most recent Form 1040 (your federal individual income tax return), and submit the complete return with Schedule C.

Total Income is not your gross receipts (your sales before expenses) and not your bank deposits. It is the figure already printed on your filed return. Schedule C is the IRS form that reports profit or loss from a business you run yourself. Keep reading to confirm which line, what to attach, and when a business loss or depreciation means you should talk to an attorney first.

Summary

For most marriage-based green card sponsors who are self-employed, the income you report on Form I-864 comes from the Total Income line of your most recent federal tax return (Form 1040, the individual income tax return), and you submit the complete return with every schedule attached, including Schedule C (the form that reports profit or loss from a business you run yourself). You report the Total Income figure, not your gross receipts and not your bank deposits. USCIS compares that figure to the 125% Federal Poverty Guidelines threshold for your household size. If your self-employment involves depreciation, a business loss, or more than one business, those situations follow rules the instructions do not spell out, and an immigration attorney should review your case before you file.

| Which figure to report | The Total Income line from your most recent Form 1040 (your federal individual income tax return), not gross receipts and not take-home cash |

| What you submit | Your complete federal tax return for the most recent year, including every Form 1040 schedule you filed (Schedule C, and any Schedule D, E, or F) |

| Schedule C | Required for a self-employed sole proprietor; it reports your business profit or loss and must be included with the return you submit |

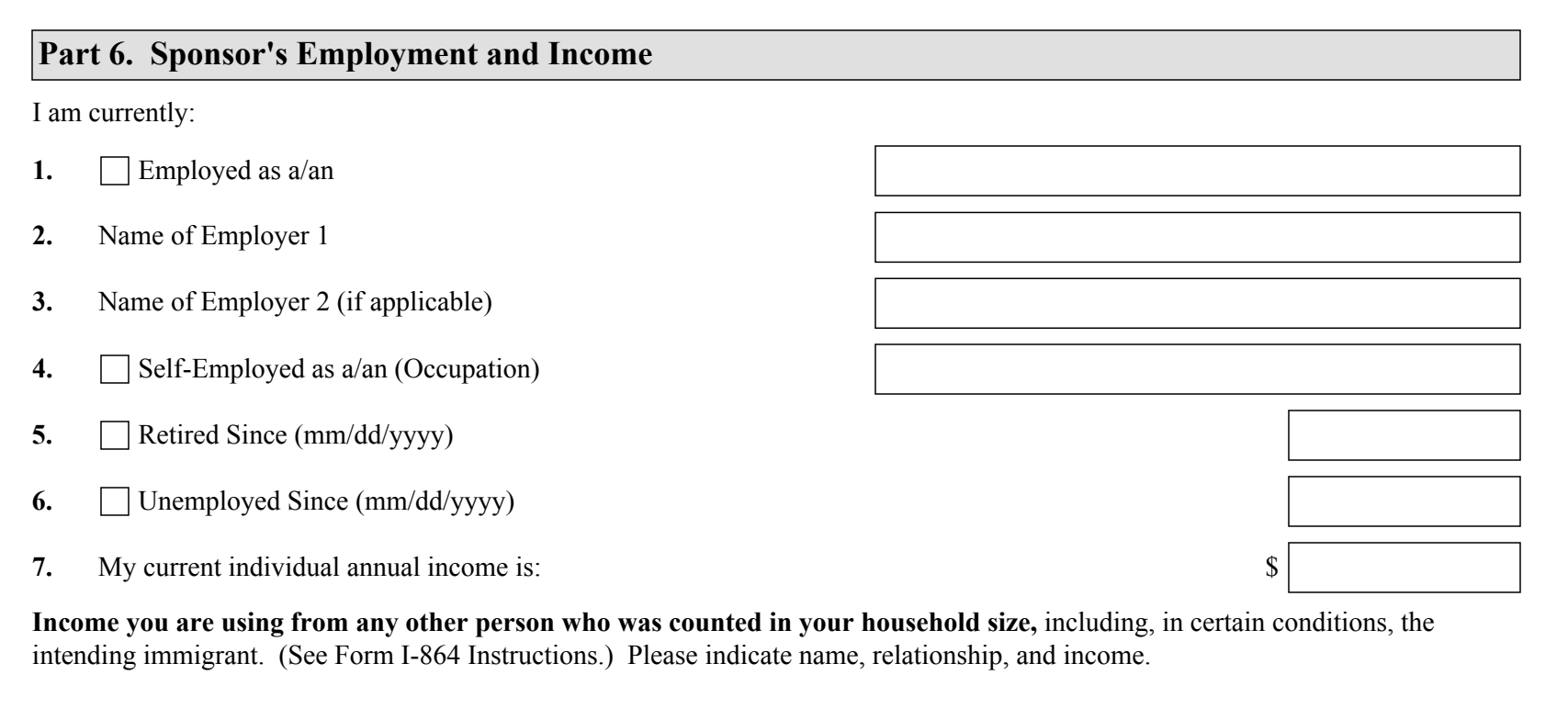

| On the form | Check Part 6, Item 4 (Self-Employed as a/an) and enter your income figure in Part 6, Item 7 (current individual annual income) |

| Tax transcript or photocopy? | Either an IRS transcript or a photocopy from your own records is acceptable; a photocopy must include every W-2 and 1099 that relates to the return |

| When to stop and get an attorney | Depreciation, a business loss, multiple business entities, or a partnership or S-corporation stake; these follow rules the instructions do not detail |

Scope of this page

This page covers a self-employed sole proprietor who reports the Total Income line from a recent Form 1040 and submits the complete federal tax return with Schedule C. If your self-employment involves a business loss, depreciation on business assets, more than one business, a partnership or S-corporation stake, primarily foreign income, or a current income figure that is not yet on a filed return, those situations follow rules the I-864 Instructions do not spell out. Consult an immigration attorney before completing Part 6.

Free tool

I-864 Income Requirement Calculator

2026 · household of 3

$34,075

Enter your household size and income to instantly check the 2026 I-864 Affidavit of Support threshold.

Free — enter your email and it opens right up. Unsubscribe anytime.

What the USCIS instructions say

The self-employed box and the income field both live in Part 6 of the form. The income figure traces to your federal tax return, covered in the instructions under Items 15-19.

Verbatim from Form I-864 Instructions, edition 10/17/24, page 11 (Federal Income Tax Return Information)

“If you selected Part 6., Item Number 2. that you are self-employed, you should have completed one of the following forms with your Federal income tax return: Schedule C (Profit or Loss from Business), Schedule D (Capital Gains), Schedule E (Supplemental Income or Loss), or Schedule F (Profit or Loss from Farming). You must include each and every Form 1040 Schedule, if any, that you filed with your Federal income tax return.”

The on-form checkbox for self-employment is Part 6, Item 4 (the instruction text refers to it as Item 2). In plain terms: check the self-employed box, write your occupation, and attach the complete return with every schedule you filed, Schedule C included.

Verbatim from Form I-864 Instructions, edition 10/17/24, page 11

“For purposes of this affidavit, the line for Total Income on IRS Forms 1040 and 1040A will be considered when determining income. For persons filing IRS Form 1040 EZ, the line for adjusted gross income will be considered.”

That sentence is the heart of it: the figure USCIS considers is the Total Income line on your Form 1040. For a self-employed sponsor, that line already reflects your business profit or loss because Schedule C flows into the 1040. You report what is on the return, not a number you rebuild by hand.

What USCIS does with this figure

USCIS compares your income to the 125% Federal Poverty Guidelines threshold for your household size from Part 5, Item 8. For a self-employed sponsor, the tax return is the primary proof, so the Total Income line and the income you state in Item 7 need to line up with what the return shows.

If your Total Income clears the threshold on its own

I-864 Instructions, edition 10/17/24, Part 6: "If your individual annual income listed in Item Number 7. is greater than 125 percent ... of the Federal Poverty Guidelines for your household size from Part 5., Item Number 8., you do not need to include any other household member's income." Items 8-14 can be left at 0.

If your Total Income falls short

USCIS moves to Part 6, Items 8-14 (household member income) and Part 7 (assets) to determine whether the combined total clears the threshold. If neither qualifies, a joint sponsor filing a separate I-864 is required. A self-employed return that shows a low Total Income, a deduction-heavy year, or a business loss is a situation to take to an attorney before you decide your next step.

What you report, and what you do not?

Report and submit

- Total Income from Form 1040: The instructions state the Total Income line on Form 1040 is the figure USCIS considers. Find that line on your most recent return and use that number for Part 6, Item 7.

- The complete federal tax return: Submit the whole return for the most recent year, either an IRS transcript or a photocopy from your records. A photocopy must include every W-2 and Form 1099 that relates to the return.

- Every schedule you filed: The instructions require each and every Form 1040 schedule you filed. For a self-employed sole proprietor that includes Schedule C; include any Schedule D, E, or F you also filed.

- Schedule C: Schedule C reports profit or loss from a business you operate yourself. It is part of the return you submit, not a separate calculation you redo by hand.

Do not report

- Gross receipts: The total amount your business brought in before expenses is not your income figure. The instructions point to the Total Income line on the 1040, which is after business expenses are accounted for on Schedule C.

- Bank deposits or cash on hand: Money moving through a business account is not the same as income. Use the Total Income line from the filed return.

- A figure you recalculate yourself: The instructions do not ask you to rebuild your business income by adjusting your tax return. Report the Total Income line that is already on the filed 1040.

- State or foreign tax returns: Do not submit state income tax returns. Do not submit foreign returns unless you were not required to file a U.S. federal return and are relying on the foreign return to show income not subject to U.S. tax.

Common confusion: gross receipts vs. Total Income

Gross receipts are everything your business took in before expenses. Total Income on your Form 1040 is a different number: it is what remains after Schedule C accounts for your business expenses, combined with any other income on the return. The instructions point to Total Income, so a self-employed sponsor uses that line, not the top-of-Schedule-C sales figure.

How do you report self-employment income on the I-864?

- 01

Pull your most recent federal tax return

Locate the Form 1040 you filed for the most recent tax year, counting from the date you sign the I-864. You will need either an IRS transcript of that return or a photocopy from your own records. Both are acceptable to USCIS.

Example: You sign the I-864 in 2026 and your most recent filed return is for tax year 2025: use the 2025 Form 1040. - 02

Find the Total Income line

The instructions state the Total Income line on Form 1040 is the figure USCIS considers. This line already reflects your business profit or loss after Schedule C carries into the 1040. Use that number, not your gross receipts.

Example: Your Schedule C shows a net profit that flows into the 1040, and the Total Income line reads $58,000: report $58,000 in Part 6, Item 7. - 03

Check the self-employed box and enter the income figure

On the form itself, check Part 6, Item 4 (Self-Employed as a/an) and write your occupation. Enter the Total Income figure from step 2 in Part 6, Item 7 (your current individual annual income).

Example: Self-employed graphic designer: check Item 4, write "Graphic Designer", and enter the Total Income figure in Item 7. - 04

Attach the complete return with every schedule

Include the whole federal tax return for the most recent year. The instructions require each and every Form 1040 schedule you filed, which for a self-employed sole proprietor includes Schedule C. If you submit a photocopy rather than an IRS transcript, include every W-2 and Form 1099 that relates to the return.

Example: Photocopy of the 2025 Form 1040 plus Schedule C and the two 1099-NEC forms your clients issued.

Current income vs. your tax-return history

- Most recent tax-return Total Income: Required. Submit the complete return for the most recent year. This is the figure the instructions say USCIS considers.

- Three most recent years (optional): The instructions let you submit transcripts or photocopies of your returns for the three most recent years if you believe additional years help establish your ability to maintain sufficient income.

- Current-year income that differs from the return: Part 6, Item 7 asks for current individual annual income. If your current self-employment income differs from your last filed return, the figure on the form and the figure on the return can differ. For a self-employed sponsor, supporting a current figure that is not yet on a filed return is exactly the kind of situation an attorney should review.

Stop here if your self-employment is anything but a simple sole proprietorship

Self-employment income follows rules the I-864 Instructions do not spell out in detail. A business loss, depreciation on business assets, more than one business, a partnership or S-corporation stake, or income that is not yet on a filed return can each change how your income is treated, and the wrong approach can sink your affidavit of support. We do not give a do-it-yourself answer for those cases. Consult a licensed immigration attorney before completing Part 6.

Common mistakes self-employed sponsors make

These errors appear on RFEs and cause adjudication delays. Each has a specific fix.

- 01

Reporting gross receipts instead of Total Income

The biggest self-employment error is entering the total your business brought in before expenses. The instructions point to the Total Income line on Form 1040, which already accounts for business expenses through Schedule C. Gross receipts overstate your income and do not match the return you submit.

- 02

Submitting Schedule C alone or leaving schedules out

The I-864 Instructions (edition 10/17/24, page 11) require each and every Form 1040 schedule you filed. Submitting only Schedule C, or only the first two pages of the 1040, is incomplete. Include the full return with all schedules.

- 03

Forgetting the W-2 and 1099 forms with a photocopy

If you submit a photocopy of your return rather than an IRS transcript, the instructions require a copy of every W-2 and Form 1099 that relates to the return. Self-employed sponsors who receive 1099s often omit them. Include each one.

- 04

Submitting a state or foreign tax return

The instructions say do not submit state income tax returns, and do not submit foreign returns unless you were not required to file a U.S. federal return and are relying on the foreign return to show income not subject to U.S. tax. USCIS works from your U.S. federal return.

- 05

Trying to recalculate business income by hand

The instructions do not ask a self-employed sponsor to rebuild income from the return. Report the Total Income line that is already on the filed 1040. If a business loss, depreciation, or multiple entities make the Total Income line look low, that is an attorney question, not a do-it-yourself recalculation.

Marriage-based filers: what a self-employed sponsor enters

In the standard marriage-based case, you (the self-employed U.S. citizen or green card holder) sponsor your immigrant spouse: a household of 2. The 2026 income threshold at 125% is $27,050/year. Your tax return is the proof, so the Total Income line and the figure in Item 7 should match what you filed. (Source: 2026 HHS Federal Poverty Guidelines, 125%, household of 2, 48 contiguous states and D.C.)

Standard case: self-employed sponsor, household of 2

Self-employed sole proprietor sponsoring an immigrant spouse only, with a recent Form 1040 whose Total Income line clears the threshold.

What sends a self-employed case to an attorney

- Your business had a loss this year. A Schedule C loss can pull the Total Income line below the threshold, and the rules for how USCIS treats a business loss are not spelled out in the instructions. Consult an immigration attorney before you file.

- You claim depreciation on business assets. Depreciation affects how net profit appears on Schedule C and the 1040. How that interacts with the income requirement is not addressed in the instructions; this is an attorney question.

- You own more than one business or a partnership or S-corporation stake. Multiple entities, partnership income (reported on Schedule E or a K-1), or S-corporation income do not follow the simple Total-Income-line rule. An immigration attorney should review your return before you file.

- Your current income is higher than your last filed return. Part 6, Item 7 asks for current annual income. Showing a self-employment figure that is not yet on a filed return is exactly the situation where an attorney can advise on what documentation USCIS will accept.

Form I-864 has many fields like this one

Our software walks through every Part 6 field in plain English, checks your income against the poverty guidelines automatically, and builds the complete packet for you to review and sign.

Start FreeRelated guides

Form and pathway context

Frequently asked questions

What income figure does a self-employed sponsor report on I-864 Part 6, Item 7?

Report the Total Income line from your most recent Form 1040 (your federal individual income tax return). The I-864 Instructions (edition 10/17/24, page 11) state that for purposes of this affidavit, the Total Income line on IRS Forms 1040 and 1040A is the figure considered. That line already reflects your business profit or loss after Schedule C, the form that reports profit or loss from a business you run yourself. Do not report gross receipts (your total sales before expenses) and do not report bank deposits.

What documents do I submit to support self-employment income on the I-864?

Submit your complete federal individual income tax return for the most recent tax year, either an IRS transcript or a photocopy from your own records. The I-864 Instructions (edition 10/17/24, page 11) require each and every Form 1040 schedule you filed, which for a self-employed sole proprietor includes Schedule C. If you submit a photocopy rather than a transcript, include every W-2 and Form 1099 that relates to the return. You may also submit returns for the three most recent years if you believe they help establish your income.

Do I report my gross business income or my net income on the I-864?

Neither phrased that way. You report the Total Income line on your Form 1040, which is the figure the instructions say USCIS considers. Total Income already accounts for your business expenses through Schedule C, so it is not your gross receipts (sales before expenses). It is the number that is already printed on your filed return, so you do not recalculate it yourself.

My business had a loss or claims depreciation. How does that affect my I-864 income?

Self-employment income involving a business loss, depreciation, multiple business entities, or a partnership or S-corporation stake follows rules the I-864 Instructions do not spell out in detail. We do not give a do-it-yourself answer for those situations because the wrong approach can sink your affidavit of support. Consult a licensed immigration attorney before you complete this field if any of these apply to you.

Can I use an IRS tax transcript instead of a photocopy of my return?

Yes. The I-864 Instructions (edition 10/17/24, page 11) accept either an IRS transcript or a photocopy from your own records, and you are not required to have the IRS certify it unless a Government official specifically instructs you to. One advantage of a transcript: if you submit a transcript, you generally do not need to attach the related W-2 and 1099 forms, while a photocopy requires every related W-2 and 1099.

I had little or no income on my last return. What do I do?

The instructions tell you not to leave the tax-year boxes blank: if the amount was zero, type or print "zero," and if you were not required to file a federal income tax return, type or print "N/A." If you were required to file but did not, you must file the late return and attach an IRS transcript or copy of it. A self-employed sponsor whose return shows little income, a loss, or a complex picture should have an immigration attorney review the case before filing.

Key takeaways

- ✓

Report the Total Income line from your most recent Form 1040; the instructions name that line as the figure USCIS considers.

- ✓

Total Income is not gross receipts and not bank deposits. It already reflects your business profit or loss after Schedule C.

- ✓

Submit the complete federal tax return for the most recent year with every schedule you filed, including Schedule C for a sole proprietor.

- ✓

A photocopy of the return must include every related W-2 and Form 1099; an IRS transcript generally does not.

- ✓

On the form, check Part 6, Item 4 (Self-Employed) and enter the income figure in Part 6, Item 7.

- ✓

A business loss, depreciation, multiple entities, or partnership or S-corporation income follow rules the instructions do not detail. Get an immigration attorney before you file.

This page is for educational purposes only and is not legal advice. Green Card Genius is self-help immigration software, not a law firm, and does not provide legal representation. Immigration law and USCIS policy change frequently. For advice on a specific case, consult a licensed immigration attorney. Form I-864, edition 10/17/24. Last verified May 2026.

Stay informed

Green card guides in your inbox

Practical, plain-English updates to help you navigate the process with confidence.

Unsubscribe anytime.

Continue reading

- 01Form I-864 Affidavit of Support: Complete 2026 Guide

- 02I-864 Current Annual Income (Part 6, Item 7): What to Enter in 2026

- 03I-864 Federal Tax Return Information (Part 6, Items 15-19): What to Enter in 2026

- 04I-864 Joint Sponsor: When You Need One and What They Must Do (2026)

- 05Marriage Green Card by Country: Country-Specific Guides (2026)

Be a Genius

Only pay when you file