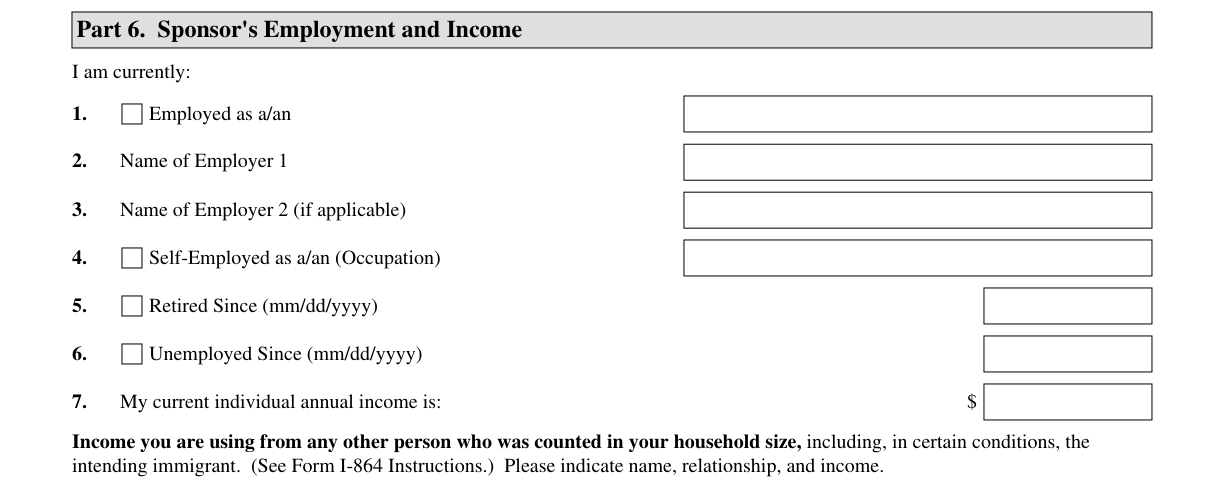

Form I-864 · Part 6, Item 7

I-864 Current Annual Income (Part 6, Item 7): What to Enter in 2026

Part 6, Item 7 is the income figure USCIS checks first. If your individual annual income clears the 125% Federal Poverty Guidelines threshold for your household size, you do not need to add household member income in Items 8-14.

Most marriage-based sponsors

Most marriage-based sponsors report their annual salary before taxes for this calendar year.

If paid hourly (full-time, 40 hours/week), multiply your hourly rate by 2,080. Do not use last year's tax return figure -- that belongs in Items 15-19. Keep reading to confirm which income types qualify.

Summary

For most marriage-based green card sponsors with regular employment, Item 7 is their annual salary before taxes for this calendar year. USCIS compares the figure in Item 7 directly to the 125% Federal Poverty Guidelines threshold for their household size from Part 5. If individual income alone clears that threshold, household member income in Items 8-14 is not required.

| What to enter | Annual income before taxes (gross income) from all eligible sources you are claiming to meet the requirements |

| Eligible income sources | Wages, salary, alimony, child support, dividends, interest, retirement income, and other lawful sources |

| Excluded | Means-tested public benefits (SSI, SNAP, Medicaid, housing vouchers, etc.) |

| Pre-tax or take-home? | Report pre-tax income (gross income) -- what your employer pays you before taxes and deductions come out, which is what an employer letter or pay stub shows |

| Evidence required? | Optional unless USCIS specifically requests it; pay stubs and an employer letter are the standard support documents |

| Why it matters | USCIS compares Item 7 against your 125% poverty guideline threshold; if it falls short, Items 8-14 and Part 7 apply |

Scope of this page

This page covers employed and retired sponsors with standard W-2 income, salary, or straightforward additional income sources (alimony, dividends, interest, SSDI). If your income is primarily from self-employment (Schedule C), a foreign employer, or a business you own, consult an immigration attorney or see the dedicated self-employed sponsor page before completing Part 6.

Free tool

I-864 Income Requirement Calculator

2026 · household of 3

$34,075

Enter your household size and income to instantly check the 2026 I-864 Affidavit of Support threshold.

Free — enter your email and it opens right up. Unsubscribe anytime.

What the USCIS instructions say

The following is verbatim from the I-864 Instructions, edition 10/17/24, Part 6, Item 7.

Verbatim from Form I-864 Instructions, edition 10/17/24, Part 6, Item 7

“Type or print your current, individual, earned or retirement, annual income that you are using to meet the requirements of this affidavit and indicate the total in the space provided. You may include evidence supporting your claim about your expected income for the current year if you believe that submitting this evidence will help you establish ability to maintain sufficient income. You are not required to submit this evidence, however, unless specifically instructed to do so by a U.S. Government official. For example, you may include a recent letter from your employer, showing your employer’s address and telephone number, and indicating your annual salary. You may also provide pay stubs showing your income for the previous six months. If your claimed income includes alimony, child support, dividend or interest income, or income from any other source, you may also include evidence of that income. However, you may not include any means-tested public benefits as income for the purposes of meeting the income requirement.”

The phrase earned or retirement names the primary income types, but the instruction then lists alimony, child support, dividends, interest, and other lawful sources as eligible too. The only income type the instructions explicitly prohibit is means-tested public benefits.

What USCIS does with this figure

USCIS compares Item 7 to the 125% Federal Poverty Guidelines threshold that corresponds to the sponsor's household size in Part 5, Item 8.

If Item 7 clears the threshold on its own

I-864 Instructions, edition 10/17/24, Part 6: "If your individual annual income listed in Item Number 7. is greater than 125 percent ... of the Federal Poverty Guidelines for your household size from Part 5., Item Number 8., you do not need to include any other household member's income." Items 8-14 can be left at 0.

If Item 7 falls short

USCIS moves to Part 6, Items 8-14 (household member income) and Part 7 (assets) to determine whether the combined total clears the threshold. If neither the individual income nor the household total qualifies, a joint sponsor filing a separate I-864 is required.

What income sources count -- and what doesn't?

Include

- Wages and salary (all employers combined): Annual salary before taxes (gross salary) or annualized hourly rate from all employers -- if you have a second job or part-time work, add those wages to your primary income

- Alimony received: Court-ordered alimony payments you receive; document with divorce decree and payment records

- Child support received: Court-ordered child support payments you receive; document with court order and payment records

- Dividend and interest income: Investment dividends and bank/bond interest; document with recent statements

- Retirement income: Pension payments, 401(k) distributions, IRA distributions, and Social Security retirement benefits

- SSDI (Social Security Disability Insurance): SSDI is not means-tested and may be included; document with Social Security award letter

- Rental income: Net rental income (rent received minus documented expenses); document with tax Schedule E

Exclude

- SSI (Supplemental Security Income): Means-tested benefit; explicitly excluded by the instructions

- SNAP (food stamps): Means-tested benefit; cannot be counted

- Medicaid: Means-tested benefit; cannot be counted

- Housing vouchers and Section 8: Means-tested benefit; cannot be counted

- TANF and cash welfare: Means-tested benefit; cannot be counted

- Household member income: Item 7 is individual income only; household member income belongs in Items 8-14

- 401(k) employer match: Employer matching contributions are not income you receive -- they go into a retirement account and cannot be added to Item 7

Common mistake: pre-tax salary vs. take-home pay

For employment income (wages, salary), report your pre-tax amount (gross income) -- what your employer pays you before income taxes, payroll taxes, and other deductions come out. That is what appears on employer letters and pay stubs. Take-home pay (the amount in your bank account) is lower and will understate your income. Rental income is different: use net rental income per Schedule E, not total rents collected.

How do you determine your current annual income?

- 01

Start with your primary income source

For a salaried employee, your current annual income is the pre-tax salary -- the amount before taxes, 401(k) deferrals, or health insurance premiums are taken out. Locate this figure on your most recent pay stub or offer letter; it is the larger number, not the take-home amount.

Example: Annual salary of $65,000 listed on your employment offer letter: enter $65,000. - 02

If paid hourly, annualize your rate

Multiply your current hourly rate by the number of hours you work per year. For a standard full-time schedule: hourly rate x 40 hours x 52 weeks = 2,080 hours. Part-time schedules use the actual hours per week. If you recently received a raise, use the new rate.

Example: Hourly rate of $22/hr at 40 hours/week: $22 x 2,080 = $45,760. - 03

If you recently started a new job

Use your current annualized rate, not last year's income from a previous employer. The instructions permit supporting evidence: an employer letter showing the employer's address and phone number, along with your annual salary, is the standard document. Pay stubs for the previous six months are also acceptable.

Example: Started new job 3 months ago at $70,000/year salary: enter $70,000 and include the employer letter. - 04

Add any additional qualifying income sources

If you receive alimony, child support, dividends, interest, or retirement income that you want to count, add those figures to your employment income. Include supporting documents for each source. The instructions explicitly state you may include evidence of alimony, child support, dividends, and interest income.

Example: Salary of $40,000 plus $6,000/year in child support received: enter $46,000 and include the court order. - 05

Do not deduct anything from employment income

For wages and salary, don't subtract anything -- not taxes, not your 401(k) deferral, not health insurance premiums. USCIS compares Item 7 to a pre-tax income benchmark for employment earnings. Note: rental income is an exception -- use net rental income (rent received minus expenses) consistent with Schedule E, not the total rent collected.

Example: Annual salary of $55,000 with $8,000 withheld in taxes: $55,000 goes in Item 7, not $47,000.

Self-employed sponsors: this page does not cover your income calculation

If your income comes primarily from self-employment reported on Schedule C, your current annual income calculation follows different rules that the I-864 Instructions do not spell out in detail. The steps above apply to W-2 employment income and do not cover Schedule C income. Consult an immigration attorney before completing Part 6 if self-employment is your primary income source.

Common mistakes on Part 6, Item 7

These errors appear on RFEs and cause adjudication delays. Each has a specific fix.

- 01

Using last year's tax return figure instead of current income

Part 6, Items 15-19 cover your prior-year tax return income. Item 7 is your current year income. If you received a raise, changed jobs, or your income has changed, your Item 7 figure will differ from your most recent tax return's total income. Enter what you expect to earn this calendar year, not what you earned last year.

- 02

Using take-home pay instead of pre-tax income

Item 7 asks for your pre-tax income (gross income) -- not what hits your bank account after deductions. Report the amount before income tax withholding, payroll taxes, and paycheck deductions are taken out. Using take-home pay understates your income and can make a qualifying income look insufficient.

- 03

Including household member income in Item 7

The word 'individual' in the instruction text is intentional. Item 7 is for your income only. Your spouse's income, a parent's income, or a household member's income belongs in Part 6, Items 8-14, not in Item 7. Including someone else's income in Item 7 is an error.

- 04

Including SSI or other means-tested benefits

The I-864 Instructions (edition 10/17/24, Part 6) explicitly state: 'you may not include any means-tested public benefits as income for the purposes of meeting the income requirement.' SSI, SNAP, Medicaid, TANF, and housing vouchers cannot be counted. SSDI (Social Security Disability Insurance) is not means-tested and may be included.

- 05

Not annualizing for recent job changes

If you started a new job two months ago, your year-to-date earnings will be low even if your annual salary is high. Annualize your current salary and support it with an employer letter and recent pay stubs. Entering only the year-to-date amount from your pay stub will understate your income.

Marriage-based sponsors: what Item 7 usually looks like

For the standard marriage-based green card case with a household of 2, the 2026 income threshold is $27,050/year at 125%. Most employed sponsors clear this with their salary alone. (Source: 2026 HHS Federal Poverty Guidelines, 125%, household of 2, 48 contiguous states and D.C.)

Standard case: employed sponsor, household of 2

U.S. citizen petitioner with regular employment, sponsoring immigrant spouse only, no additional household members contributing income.

What changes your Item 7 figure

- Received a raise this year. Use the new rate, not last year's W-2 figure. Document with a recent pay stub or employer letter showing the new salary.

- Started a new job recently. Annualize your current rate. Include an employer letter. Do not average your income across a job transition.

- You receive additional income (alimony, dividends, child support). Add those amounts to your salary figure. Include supporting documents for each additional source.

- Part-time or seasonal employment. Annualize based on your actual expected hours for the year. If income is irregular, consider whether your household income (Items 8-14) or assets (Part 7) are needed to supplement.

Form I-864 has many fields like this one

Our software walks through every Part 6 field in plain English, checks your income against the poverty guidelines automatically, and builds the complete packet for you to review and sign.

Start FreeRelated guides

Frequently asked questions

What documents do I submit to support Part 6, Item 7 of the I-864?

Supporting documents are optional unless USCIS specifically requests them, per the I-864 Instructions (edition 10/17/24, Part 6). The standard documents are: a recent employer letter showing the employer's address, phone number, and your annual salary; and pay stubs covering the previous six months. If you also claim alimony, child support, dividends, interest, or rental income, include evidence for each additional source -- court orders, statements, or tax schedules as applicable.

Should I enter my pre-tax salary or my take-home pay in Part 6, Item 7?

Enter your pre-tax salary -- the full amount your employer pays you before taxes and other deductions come out (also called gross income). Do not enter your take-home pay (the amount deposited in your bank account). Employer letters and pay stubs both show the pre-tax figure. USCIS compares Item 7 to the Federal Poverty Guidelines, which are expressed as pre-tax income benchmarks. Using take-home pay understates your income.

I just started a new job. How do I calculate my current annual income?

Use your current annualized salary or hourly rate, not the year-to-date total on your pay stub. For a salaried employee: use the annual salary shown on your offer letter or pay stub. For an hourly employee: multiply your current rate by 2,080 (40 hours per week times 52 weeks). Support your claim with an employer letter stating your annual salary and recent pay stubs, as described in the I-864 Instructions (Part 6).

Can I include rental income, dividends, or interest in Item 7?

Yes. The I-864 Instructions (edition 10/17/24, Part 6) state that you may include alimony, child support, dividend or interest income, or income from any other source. For rental income, use net rental income (rent received minus allowable expenses), which aligns with what appears on your tax return Schedule E. Document each source with recent statements or tax schedules.

Can I include Social Security disability benefits in Item 7?

It depends on the type. SSDI (Social Security Disability Insurance) is not a means-tested benefit and may be included in Item 7. Document it with your Social Security award letter. SSI (Supplemental Security Income) is means-tested and explicitly excluded by the I-864 Instructions (edition 10/17/24, Part 6), which state you may not include any means-tested public benefits. If you are unsure which type you receive, check your Social Security benefit statement.

What is the difference between Item 7 (current income) and the tax return income in Items 15-19?

Item 7 is your projected current-year income. Items 15-19 capture what you reported on your most recent federal tax return. These figures can differ: you may have received a raise, changed jobs, or have income sources that were not on last year's return. USCIS reviews both. Item 7 reflects what you expect to earn this year; your tax transcript or photocopy confirms your recent filing history. If your current income is higher than last year, supporting documents (employer letter, pay stubs) explain the difference.

Key takeaways

- ✓

Item 7 is current-year individual income, not last year's tax return total. The annualized current salary or rate is what goes here.

- ✓

Pre-tax income (the full amount before taxes and deductions are taken out) is what USCIS measures against the poverty threshold -- not take-home pay.

- ✓

New employees: annualize the current rate and include an employer letter. The year-to-date figure from a pay stub understates income if the job started mid-year.

- ✓

All lawful income sources except means-tested public benefits are eligible. This includes wages, alimony, child support, dividends, interest, retirement income, and SSDI.

- ✓

SSI, SNAP, Medicaid, TANF, and housing vouchers are means-tested and cannot be included.

- ✓

If Item 7 alone meets the 125% household poverty guideline threshold, Items 8-14 are not required.

This page is for educational purposes only and is not legal advice. Green Card Genius is self-help immigration software, not a law firm, and does not provide legal representation. Immigration law and USCIS policy change frequently. For advice on a specific case, consult a licensed immigration attorney. Form I-864, edition 10/17/24. Last verified May 2026.

Stay informed

Green card guides in your inbox

Practical, plain-English updates to help you navigate the process with confidence.

Unsubscribe anytime.

Continue reading

- 01Form I-864 Affidavit of Support: Complete 2026 Guide

- 02What If the Petitioner's Income Is Too Low? Joint Sponsor Options

- 03I-864 Income Calculator: Green Card Affidavit of Support (2026)

- 04I-864 Part 5, Item 1: Total Number of Persons in Household (2026)

- 05I-864 Affidavit of Support: Field-by-Field Guide (2026)

Be a Genius

Only pay when you file